All eyes on the US – or not

As President Trump’s second term begins, the outlook for New Energy markets in the United States presents a mixed picture. Some sectors, such as carbon capture and blue hydrogen and ammonia, are likely to experience modest growth. Other areas of New Energy like offshore wind and Power-to-X are expected to face significant headwinds under the Trump administration’s policies.

The US green low-emission sector remains largely stagnant, hampered by delays in key regulatory guidance. Many projects were waiting on the Department of Treasury rules on 45V tax credits, which was released in January 2025 – only weeks before the incoming administration’s inauguration.

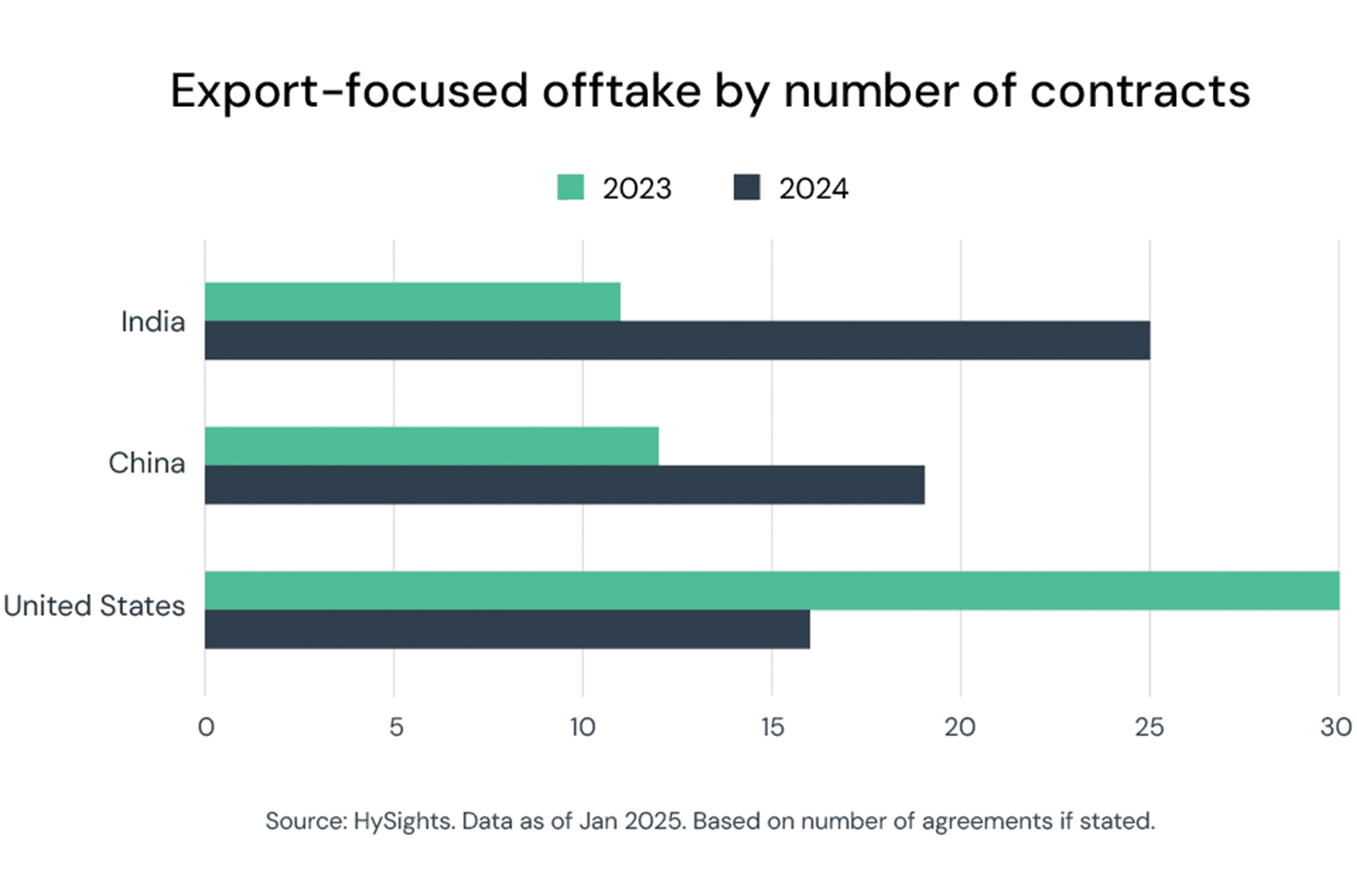

The number of offtake agreements for low-emission fuels from the US, such as hydrogen, ammonia, and methanol, has declined sharply from 30 in 2023 to 14 in 2024, according to HySights data. Meanwhile, India and China have emerged as leading sources for these fuels.

While US blue hydrogen projects may benefit from increased natural gas availability under the Trump administration’s pro-drilling policies, challenges persist. European buyers remain cautious due to ongoing legislative deliberations over emission intensity definitions and upstream methane accounting. Additionally, offtakers in North Asian markets looking for blue projects have the nearer option of Middle Eastern suppliers.

Strengthening transnational cooperation

Multinational agreements continue to play a pivotal role in scaling low-emission markets. While country-to-country agreements often appear high-level and aspirational, some demonstrate tangible impact.

Germany’s H2Global was particularly active and exemplified effective bilateral cooperation in 2024. The programme secured significant commitments from Canada (C$300 million) and Australia (€200 million) to support future joint tenders. Moreover, H2Global has entered into a partnership with India’s Solar Energy Corporation, which runs contract-for-difference tenders to stimulate market development.

Given the high price differential between low-emission and conventional fuels, government subsidies and international cooperation are essential to market growth. National-level MoUs should be watched for attentively.

In 2025, H2Global’s implementation arm, Hintco, is set to launch up to five targeted buy tenders, including a global lot, with a budget of €3 billion.

Further transnational cooperation is needed. In particular, the differing definitions of low-emission standards and carbon accounting across different locations need to be clarified and standardised. This is vital for reducing barriers and to facilitate growth in these New Energy markets.

Growth in shipping and aviation

The implementation of EU consumption mandates in 2025 marks a turning point for hard-to-abate sectors like aviation and shipping. These regulations will require increased use of sustainable aviation fuel (SAF) and low-emission bunker fuels.

At present, most airlines and shipping companies are not prepared to meet these requiremetns for the 2026-2030 period. And given that ReFuelEU Aviation and Shipping regulations apply to sectors that are inherently global in scope, their effects are expected to be felt across markets worldwide.

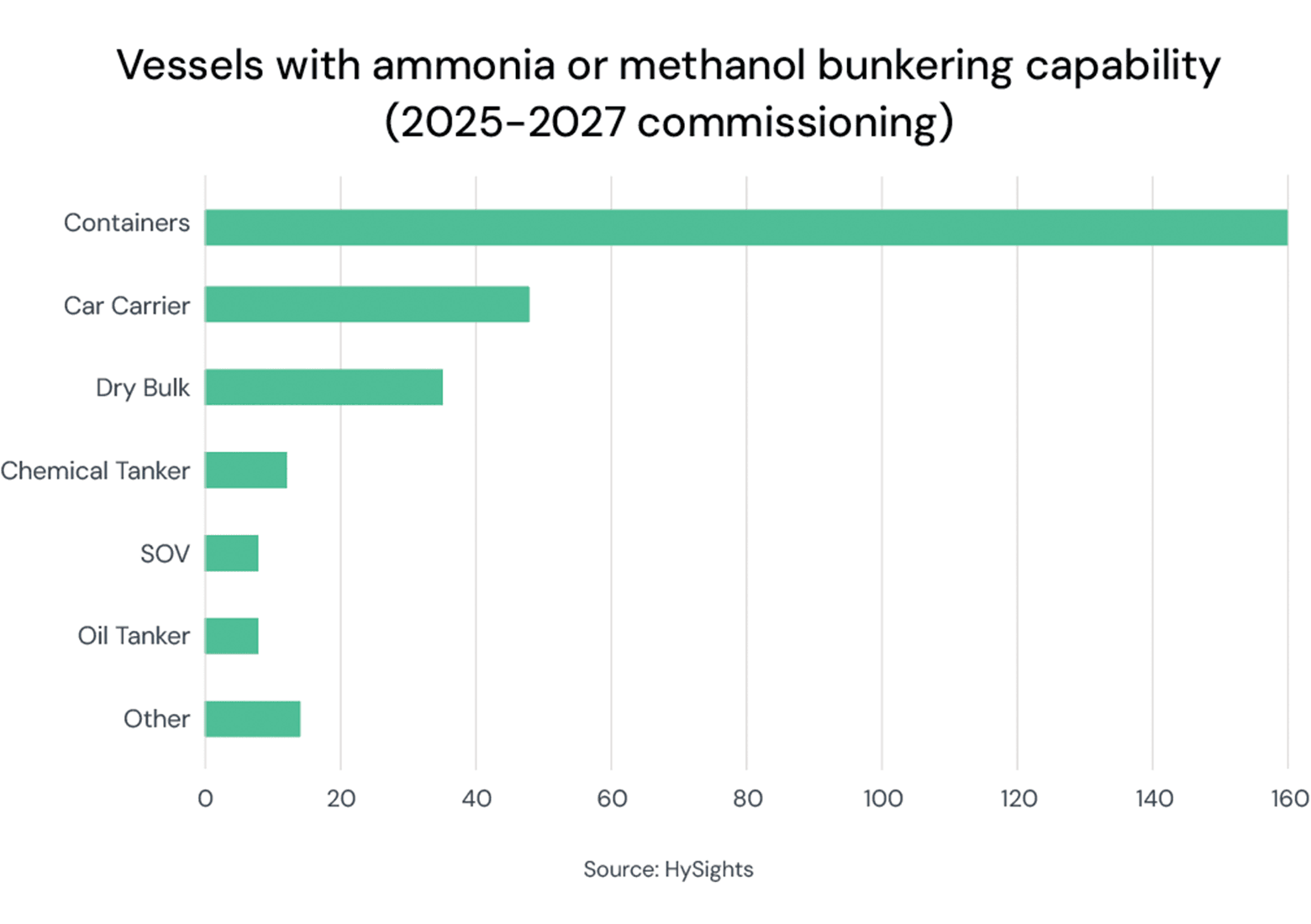

In shipping, over 285 large-scale vessels (either containers, dry and wet bulk, or car carriers) that can use low-emission bunker fuel are expected to be delivered between 2025 and 2027. However, many shipowners lack sufficient offtake agreements for ammonia and methanol, which sets the stage for increased contracting activity in the space. European maritime-focused projects are also well-positioned to receive €200 million in grants from the next European Hydrogen Bank auction, further driving activity.

China is the likely major supplier of these low-emission bunker fuels, given its strategic location along major shipping routes and its still unsold production of ammonia and methanol – projected at 600,000 tonnes over the next two years from projects targeting shipowners as end users.

In aviation, the EU’s 5% SAF mandate by 2030 has created an urgency for airlines to significantly ramp up procurement. Current deals primarily favour bio-SAF over e-SAF due to lower costs and greater availability. However, e-SAF’s significantly higher hydrogen requirements – up to fourteen times that of bio-SAF – point to its potential role in driving hydrogen demand over the longer term.

Bio- outmuscling e-

The preference for bio-based fuels over synthetic alternatives remains evident across sectors. For aviation and shipping, bio-based SAF and methanol solutions are attractive primarily because of their immediate or near-term availability. Cost is the other important factor.

The first large-scale bio-SAF refineries started operating several years ago, and new bio-SAF facilities in countries like Thailand and South Korea further strengthen the case for bio-based solutions.

In contrast, e-SAF and e-methane continue to face challenges. While e-SAF saw offtake traction in the US thanks to IAG, one of the world’s largest airline groups, its costs are two to three times higher than its bio-based counterpart. Nonetheless, European regulations mandate that airlines will need to have a portion of e-SAF in their fuel mix.

The debate between bio-based and synthetic fuels has also gained prominence in the gas sector, with bio-methane and bio-LNG positioned as emissions-reducing, marginally premium alternative for bunkering, power generation, and heavy industry.

The scalability of bio-LNG is evident, with production levels sufficient to support shipping in conventional vessels. For instance, Mitsui demonstrated the viability of bio-LNG in early 2024, while Singapore’s Maritime and Port Authority (MPA) recently issued an Expression of Interest (EoI) for a supply of bio-LNG to support bunkering activities. Similarly, shipping giant Maersk has integrated bio-LNG into its strategic roadmap, placing orders in 2024 for 22 LNG dual-fuel containerships.

Meanwhile, e-methane remains largely at the conceptual stage, with very little firm offtake. Initiatives from Japanese and US companies promoting the potential of e-methane as a substitute for fossil methane – thereby avoiding significant midstream disruption – make a sound logical case, but at a cost of three-times even biomethane, e-methane has some way to go to become competitive.

Renewed tender activity

Tender activity in 2024 fell short of expectations, with several programmes underperforming. South Korea’s inaugural Clean Hydrogen Production Standard (CHPS) tender awarded only about 10% of its potential volume, while Germany awarded only the green ammonia portion of its buy tender. Japan delayed its tenders to the end of its financial rather than calendar year, and numerous within-country tenders from a mix of private and public entities were either unannounced or were unawarded.

The outlook for auctions and tenders (and other subsidy-awarding exercises) in 2025 is more optimistic. Singapore plans to conclude its tender for ammonia use in power generation and bunkering by mid-2025. South Korea is expected to issue a follow-up CHPS tender, while Japan’s contract-for-difference scheme is expected to yield several project awards. Additionally, the European Hydrogen Bank’s second auction, with nearly €2 billion to award, should announce results in the first half of 2025.

These tenders and auctions are expected to provide much-needed clarity and financial support for both large-scale and smaller projects, shaping the future of low-emission hydrogen and ammonia markets.

Learn more about HySights Ratings

To request a demo or HySights Ratings methodology, reach us at contact@hysights.com

Access market insights