Key takeaways from Australia’s Renewable Fuels Summit 2026

While resource-rich and historically a net exporter of raw materials that are upgraded elsewhere, Australia is also a large country with significant regional differences: States such as Western Australia and Queensland have made the country one of the world’s largest LNG exporters while others like New South Wales and Victoria face shortages of domestic gas.

There is a opportunity for biogas energy production to address these supply gaps while contributing to reductions in carbon dioxide-equivalent (CO2e) emissions. At present, biogas production is maturing but has yet to take off.

Since the Paris Agreement in 2016, Australia has pursued an ambition to not only become a world-leading fossil fuel producer and exporter, but also one of the largest renewable energy producers and exporters. And given its vast landmass as well as ample solar and wind resources, Australia appeared well-positioned to become the next green energy powerhouse.

How Australia’s hydrogen ambitions faltered

Australian federal and local governments had moved to legislative frameworks for hydrogen production and exports, partnered with industry to speed up the development of mega hydrogen projects, and committed substantial development subsidies with promises to build key infrastructure enabling its use and exports.

These efforts however encountered significant headwinds: The demand for hydrogen products and its number of end-use applications fell short of expectations. Hydrogen equipment performance lagged behind that of the competition and production costs in Australia were much higher than anticipated.

Specifically, Australia’s green hydrogen ambitions could not sufficiently overcome:

- Higher electricity demand from higher willingness-to-pay sectors, such as digital infrastructure

- Longer planning and permitting rules than most countries

- Higher labour costs and environmental hurdles

- A lack of vertical integration advantages for technology or end-use

Ammonia away

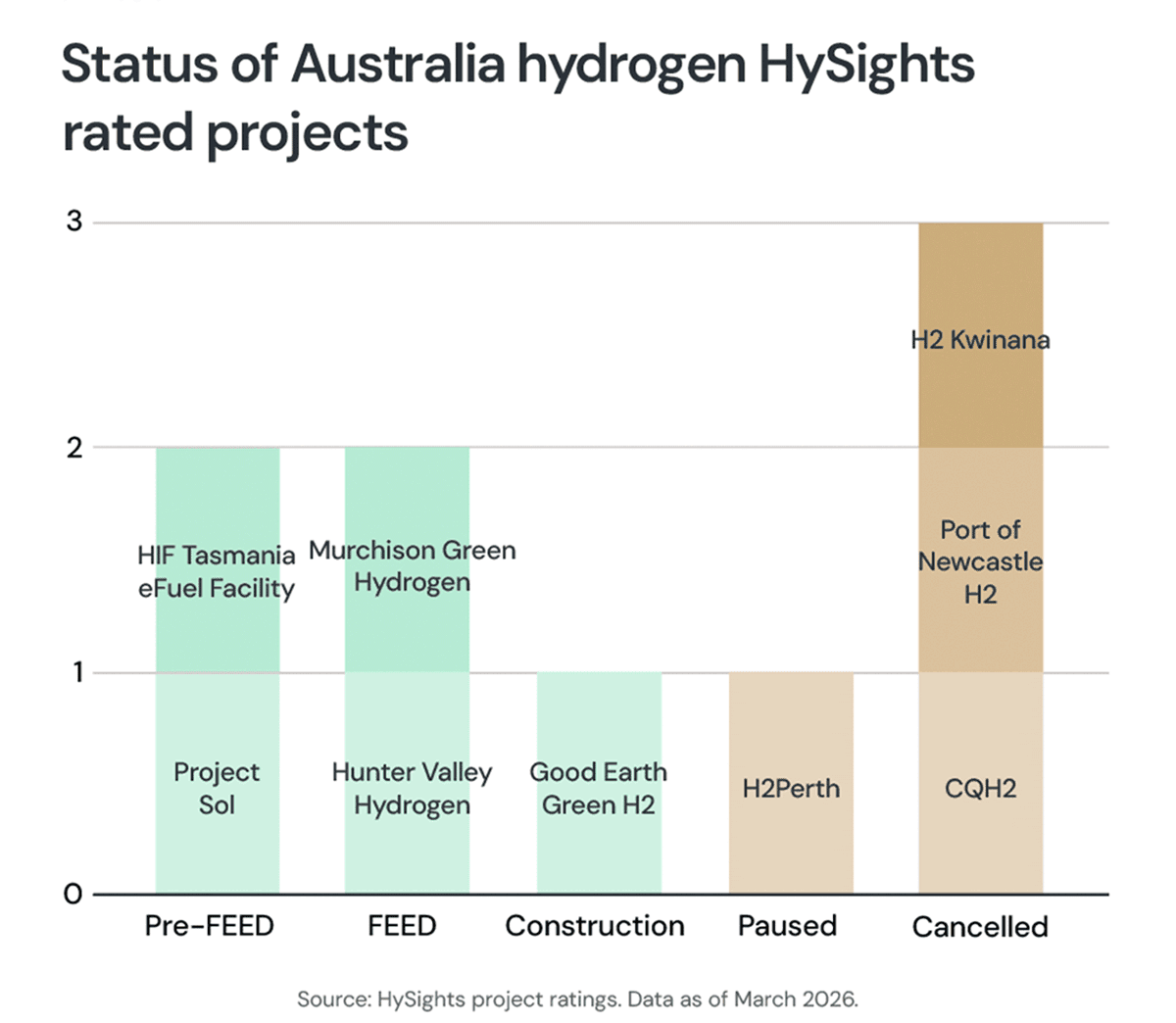

Per Figure 1, cancelled Australian projects are mainly large-scale, export-oriented ammonia projects. Projects that remain active or under construction are locally-led, heavily-subsidised and small – too small to make a significant carbon reduction impact.

SAF on the up

Broader ambitions have given way to more targeted strategies with remaining hydrogen projects either “hedging” – offering data centre development on their land – or pivoting to different outlets.

One such outlet is the use of hydrogen in Sustainable Aviation Fuel (SAF) through the Alcohol-to-Jet route, where hydrogen is used to increase the efficiency of biomethanol production. This route is gaining traction as demand for renewable methanol originally intended for the maritime sector is weakening. HAMR Energy, who recently raised a Series A with Boeing and Qantas as investors, is a notable example of this strategic pivot and how developers are progressing with renewable fuel production.

Green steel: Deferred, not abandoned

Australia’s dominant position in iron ore production made “green steel”, or hydrogen-derived hot briquetted iron, a logical growth area for hydrogen use. However, renewable hydrogen prices remain prohibitive in Australia, and the country does not currently produce DR pellets – the high-grade pelletised iron ore required for the process, now largely sourced from Brazil or Sweden.

In all, Australia’s green steel ambitions are said to be on hold, rather than permanently paused.

Renewable gases: The next wave

While biogas has emerged as the next viable option for Australian users and industry to decarbonise, production economics present a significant barrier: the production cost for biogas or biomass-derived liquid fuels are much higher than their fossil equivalents.

HySights expects the first wave of biomethane – compatible with Australia’s extensive gas pipeline system – will be developed by greenfield asset management platforms and the few existing biogas developers in the country. Based on HySights interactions with energy majors at the Summit, they are unlikely to be first movers, citing concerns over policy consistency and technology and market risks.

The first users are most likely to be based abroad, with Japan, South Korea, and Singapore as the three main contenders. These countries seek to leverage Australia’s supply through existing LNG facilities in Queensland, Northern Territory or Western Australia, and view Australia as a politically neutral supply partner and ally.

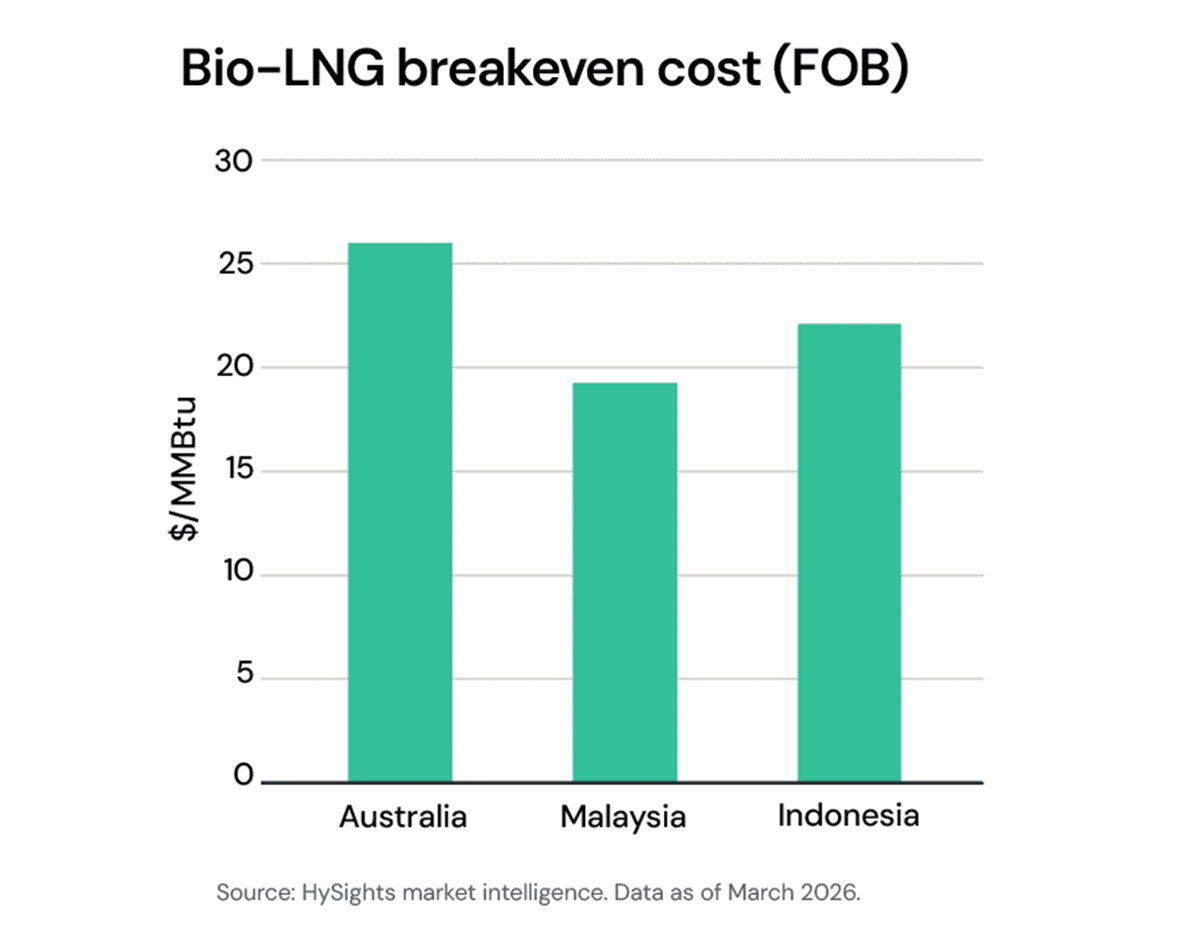

Australia’s biomethane and bio-LNG projects will need to bank on energy security encouraging a higher willingness-to-pay as their bio-LNG remains less competitive than Malaysia or Indonesia even by using existing large-scale liquefaction facilities.

Regulatory fragmentation, policy uncertainty

The Australian federal government’s policy focus on hydrogen has left bioenergy without a regulatory framework, mandates or support mechanisms. Compared to Europe and the United States, the fundamentals for a large-scale roll-out of this renewable fuel industry are either absent or underdeveloped.

Combined with domestic consumers’ low willingness-to-pay from domestic consumer, this creates a challenging environment for the industry. Integrated energy companies monitoring the sector closely have cautioned that the bioenergy industry risks following a trajectory similar to hydrogen. By their account, these missing fundamentals mean that the scale-up of biogas and biofuel production, which requires hundreds of millions dollars in investment for a larger-scale plant, will be too risky.

Not all states have followed up on federal directives for biomethane injections into the natural gas grid as well. Western Australia, for instance, does not allow the chemically identical biomethane in the natural gas grid as it is not of fossil origin. Additionally, there is a lack of clear direction on policies for the designation of carbon certificates for renewable gases. While foreign buyers are offering the highest profit margins for developers, there is no established regulation around the export of biomethane.

The last key issue is the absence of internal market to form the basis of the industry, given the price sensitivity of Australians and the lack mandates. As such, the required capital is expected to flow to other countries where these elements are in place.

Gas and fuel have always been politically fraught in Australia, and this won’t be any different if it’s derived from biomass.

– Strategy Executive, Global Energy Major

Positive signals

New South Wales (NSW) released a grant of AU$60 million for renewable gas from agricultural waste and has set a renewable gas blending mandate in place with a penalty of AU$10.5 per GJ. This demand mandate, along with the supply-side subsidy scheme launched by the Federal Government (the federal renewable fuel fund of AU$1.1 billion), corporates that are willing to absorb price premiums to reduce their scope 1 emissions, and more importantly an industry with ample projects in the pipeline, are positive signs for the ecosystem.

More progressive project developers and energy companies acknowledge that the governmental framework is weak, but see this as quickly changing. In their view, the government has heard the call for action and is shaping this in close collaboration with industry, taking lessons from other countries such as the UK and the EU.

Liquid biofuels: A national security issue

Currently 80% of Australia’s liquid fuel supply is imported, making the development of the country’s domestic biofuel production a matter of fuel security and resilience. Australia’s Department of Defense is actively investing in applications for SAF and looking for the offtake of “homegrown” jet fuel. Qantas and Sydney Airport are working together to invest in Australia-based SAF projects to achieve their internal SAF usage targets and to diversify sourcing.

The test of resilience will come sooner than expected: the Iran conflict has disrupted global energy supply chains, with China temporarily suspending export permits for its oil-based fuel exports – from which Australia imports 32% of its jet fuel. Without this, Australia will need to turn to its other suppliers, like reloading from Singapore and Jet A-1 produced in South Korea, that are short in supply of feedstocks themselves.

In all, an East-of-Hormuz autarky push is taking off in earnest and Australia’s local biofuels industry could be a major beneficiary. However, it remains up to the Australian government to ensure that the fundamentals are in place and the consumer convinced to pay a premium for sustainability and resilience. And while the industry is ready to move, early movement is not expected from the large international integrated energy companies but from developers specialised in bioenergy and newfound fuel producers.

Learn more about HySights Ratings

To request a demo or HySights Ratings methodology, reach us at contact@hysights.com

Access market insights